The road less travelled?

The road less travelled?

MBAs and Billionaires

“What this data shows is that (…) there are market inefficiencies to be exploited by MBAs who are interested in pursuing extreme wealth and willing to take less popular paths to get there” - Verdad

Some time ago I came across an interesting article by Daniel Rasmussen, Founder of Asset Management Firm Verdad, coauthored with “rising senior at Yale” Nicholas Rice. The essay is a short read and can be found here. The basic question it focuses on is how MBAs choose their careers in trying to optimize wealth. They rely on two basic assumptions: that MBAs want to get rich, and that MBAs should look towards Billionaires, the richest people in the US, to figure out they got to be that rich. These assumptions may not be perfectly true, but reasonable enough to look into the issue further.

The authors use statistics on the percentage of billionaires in different industries, such as tech, healthcare, private equity, venture capital etc. and compare them to statistics showing which industry MBAs enter after the graduation. Based on these statistics, they create the following Matrix:

Based on this, they argue that even when accounting for transitory industries, like consulting and investment banking, MBAs make a systemic error choosing industries where less billionaires built their wealth, such as consulting or healthcare, colored red in the matrix. They forego industries where a lot of billionaires are present, such as manufacturing, or Media and Telecom, colored green in the matrix.

The authors then cite statistics for specific cases, such as the overrepresentation of MBAs compared to billionaires in different sectors:

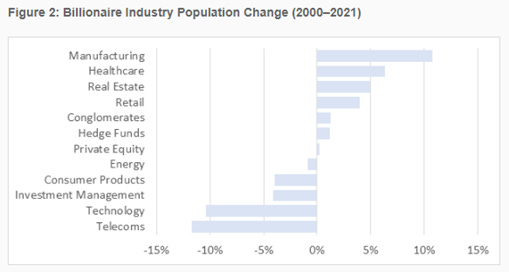

This supposedly showcases the mistakes of MBAs in their career choices. Take Manufacturing for example. Based on the authors argument, more MBAs should join this industry, as the percentage of billionaires is much higher than that of MBAs entering (6% to 0.8%). The authors continue by showing the population change of billionaires from 2000 – 2021:

They use this as further base for their argument that MBAs choose the wrong industries to attain billionaire status, if we assume that that is what they are going for. Continuing with the manufacturing example, from this graph it seems that manufacturing is the perfect industry to enter right now, based on few other MBAs entering and a large increase in billionaires over the last 20 years. Later, the authors hypothesize that MBAs choose careers that are “well suited for cocktail party conversation” or that compensation could be a factor, noting that salary ranges are $150-167.5K in consulting and finance, but only $140K in retail, $150K in telecoms and $142.5K in manufacturing. A final argument was that MBAs seek to maximize skill acquisition in advisory roles before entering a specific industry, explaining the high numbers for consulting and investment banking. They conclude with the opening quote, that there are market inefficiencies to be exploited by MBAs who are interested in pursuing extreme wealth, if willing to take less popular paths.

But their research ignores an important aspect of the real world: dynamism. Things change. Their 2 stated assumptions are relatively fine, but a crucial third on they omitted: that if an industry has a high level of billionaires at the moment, the chance to become a billionaire is also higher. The entire research is based upon this idea, yet it makes virtually no sense. If there was a correlation between, the two, I would expect it to be negative: a higher level of billionaires leads to a lower chance of becoming a billionaire in that industry going forward.

A sector with a lot of current billionaires implies that opportunities in this sector were already exploited and capitalized, and that a high level of competition in that sector already exists. If on the other hand a sector has few billionaires, it may mean that a lot of opportunities are left to uncover, that an enterprising person can built an empire with less competition by established firms. There may be a lot of billionaires in the Hedge Fund sector, but wouldn’t that make it much harder to stand out as a newcomer, attract capital and compete with the industry titans? Are they not billionaires because for decades they have proven themselves the superior business? The idea that the level of billionaires in an industry predicts the likelihood of becoming one yourself in an industry seems ridiculous.

Equally so, using historical data of the past two decades to supplement any research makes little sense. The cause of this change is of actual interest, yet never mentioned in the research. Did manufacturing gain so many billionaires because the sector is growing, because an innovative technology lead to increased profits, because new disruptors emerged? Or is it because the manufacturing bases were shifted to low-cost countries, but no new innovation happened? The research never answers this. Worse yet, a time span from 2000-2021 was a very unfortunate choice. The stark decline in tech billionaires seems incredibly surprising, given the sectors rise to the top of much of our daily lives and the incredible value of some companies within the sector. That is, until one remembers that 2000 was the literal top of the tech bubble, where unprofitable startups were worth billions and everyone in Silicon Valley was a millionaire on paper. Thus, the change in billionaire population, while it looks interesting, has little actual answers to be derived for the research question.

Finally, the research makes little sense for anyone hoping to one day become a billionaire. When trying to use statistics to maximize one’s odds of becoming a billionaire, pursuing an MBA already seems the wrong start: only 13% of billionaires have MBAs. Apart from this, there are an infinite number of variables the research never looks into: background, connections, luck. While its truly impossible to account for all these variables, drawing the conclusions the authors did out of very limited statistics is bewildering, especially considering the analytical career background they have. Statistics are about a large number of observations, largely unable to predict one person’s definite future. Nobody has a great probability to win at the casino, yet every day someone does. Similarly, nobody has a great probability to be a billionaire, roughly 1:3.000.000, and of those who are, I am sure nobody relied on statistics to get there. They rather looked to build a product with a strong market fit and scaled the business, instead of letting percentages decide the industry they enter.

Those who rely purely on statistics to make career choices will sooner or later be unpleasantly surprised. They use historical data to forecast the future. But past performance does not indicate future success. Sometimes there is a great leap, a new innovation, a new industry, which cannot be predicted by anyone, but most often leads to the greatest of fortunes. The wealthiest people in the late 1800s all came from railroads: Carnegie, Vanderbilt, Gould. Yet Ford didn’t make his fortune laying tracks.