One mans gain is a nations loss

One mans gain is a nations loss

Taxes and how not to pay them

„In this world nothing can be said to be certain, except death and taxes” – Benjamin Franklin

A lot of the work in finance and accounting involves lowering the taxes a corporation has to pay. In the end, it has the same effect as slashing other costs of the business or increasing revenue. After all, wouldn’t you pay someone $150 million if it can save you $1 billion in costs?

(The amount paid by former Apollo CEO Leon Black to Jeffrey Epstein, apparently for tax advice)

There are two main ways to lower the taxes one has to pay. Lower the tax base or lower the tax rate. To lower one’s tax base effectively means to lower the income one has to pay taxes on. For a business, this is the Earnings before taxes. It is already lessened by all the operating and financial costs of the business, such as paying staff, paying interest and paying for goods used in production.

It also includes measures like depreciation, specifically designed for the purpose of lowering taxes. It does so by capturing the effect of the wearing out of equipment over its useful life. Instead of recording the cost of buying the equipment when it is purchased, and thus lowering the tax base in that particular year, its value is slowly lowered every year. Even though no direct payments regarding the equipment are made in subsequent years, the cost of its usage is recognized and lowers the tax base in those years as well.

Sometimes, businesses will have a particularly bad year of sales, for example cinema operators during the pandemic. If their revenue decreases enough, they may end up with negative income for the year, leaving them to pay no taxes at all. An example of this was AMC in 2020, the income tax for the year was negative $4 million ( which it can carry forward into the next years to offset future taxes)

This can also be the case if there is an asset that lost a lot of its value in a year, requiring a write-down. Lowering the assets value is equivalent to a sudden, one-time cost for the business, which lowers its overall taxable income. One example of this is Warner Bros. cancelling the Batgirl and Scooby Doo movie, allowing for a roughly $130 million write-down. While there may have been more reasons for the cancellation, lowering the tax base by $130 million is not to be overlooked.

The other way to pay less taxes is to lower the tax rate. You could do so by moving the headquarters of a corporation or establishing subsidiaries into a country with a lower tax rate, such as Ireland or Hungary. But there can be a lot of headaches involved in these actions, as complexity and regulations of multiple countries are involved.

Another way is to lower the tax rate in your own country. This will of course cost you upfront: a political and media campaign to publicize arguments on why they need to be lowered. Effectively, you need to convince the public, or at least the politicians, that lower corporate taxes will benefit them. But often enough, this strategy works out just fine, as seen with the corporate tax rate being slashed from 35% to 21% by the Trump administration.

But then again, lowering corporate taxes will increase the profit for your company, but if you personally want to access this money you have to pay it out to you as ordinary income. This income will be taxed at the income tax rate, which in the US progressively increases until 37% for taxable income in excess of $500.000 annually. This rate applies for a salary, but a large part of income of ultrawealthy is the sale of assets that they possess.

For income from these sources, the applicable tax rate is capital gains tax, divided into short term and long-term capital gains taxes. Short term means that the asset has been held less than a year, whereas long term means the duration between purchase and sale of the asset is at least 366 days. The distinction here is significant, short term capital gains tax maxes out at 37% above roughly $500 thousand, but long-term capital gains max out at 20%. This means that a gain on assets held for more than a year is taxed at almost half the rate. Put another way, if you have a capital gain of $10 million before taxes, if its short term you ultimately only receive $6 million, but a long-term capital gain would allow you to keep $8 million.

High earners love this distinction, it allows them to capture 1/3 additional value. And through loopholes and dedicated lobbying, investment managers have for decades been able to classify their income as long-term capital gains in what is known as the carried interest loophole. Those managers usually receive a performance fee, around 20% of the profit they make for investors in a given year, which is taxed not as income but long-term capital gains if part of an investment held long enough. A practice long criticized by both parties; even Trump wanted to end it; it survived the latest attack when Senator Kyrsten Sinema objected to a provision in the Inflation Reduction Act.

But what if your income truly isn’t long term capital gains? Do you suck it up and pay double the tax rate that your other billionaire friends are paying? Of course not. You did not become a billionaire by bending over and playing by the rules. You find savvy ways to circumvent them, at least temporarily, if worse comes to worst you at least put up a fight with the government to get your hard-earned money.

Such is the story of Jeff Yass (described in detail by ProPublica), billionaire founder of Susquehanna International Group. SIG is a market maker in financial markets, meaning it makes money by providing liquidity and finding arbitrage. It is not directly in the business of betting on the direction of a singular stock, or the stock market as a whole, but rather facilitating transactions and finding inconsistencies. In the course of this business, it does not take positions for very long, certainly not for a year or more. Therefore, most of the income Mr. Yass earns would be in the form of short-term capital gains, from the purchase and subsequent sale of assets. But what if you could transform this income into long term capital gains, paying half the tax rate?

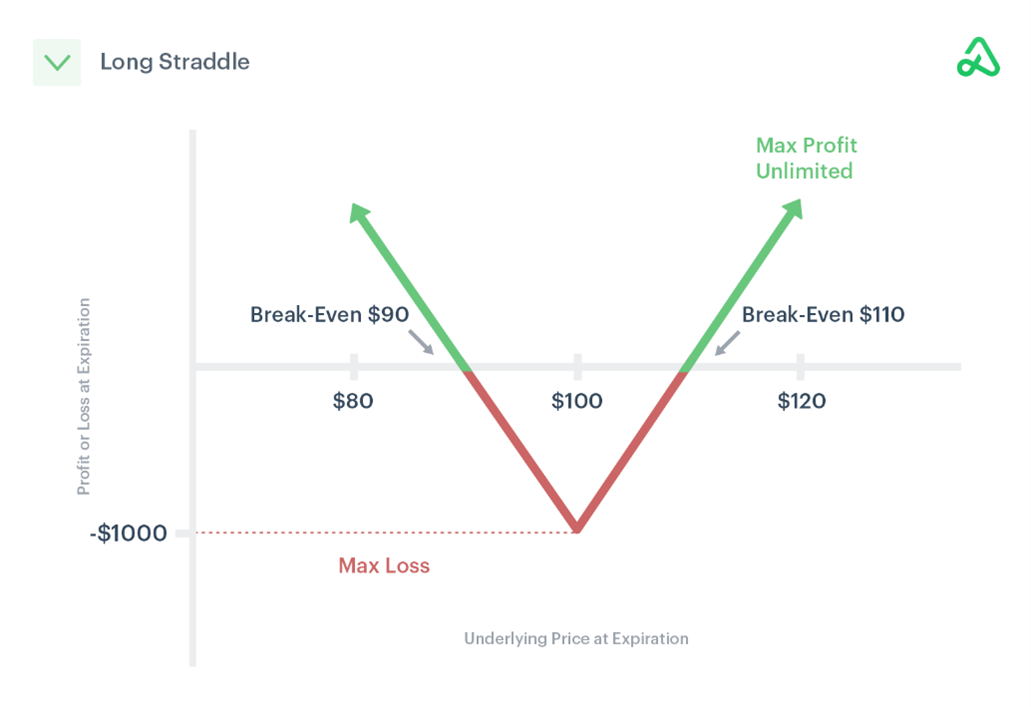

The basic strategy to do this is called a straddle. It is traditionally an option strategy in which a trader buys a put and call option on the same underlying with the same strike price. The potential profit is due to the leverage of options, ideally one of them will be worth 0 and the other one will have increased in value multiple times:

But it can also be used on normal shares. Since there is no leverage in this situation, the payout would be equal to zero. You short a share and buy one simultaneously. For every increase or decrease in the share price, the two positions cancel out. (Technically you need to pay a borrow fee, but this will be very small and irrelevant for this example.) Now this seems rather pointless until now.

But the true value is from selling these positions at different times. Whatever position is currently negative, you sell after exactly 365 days. If your position in the stock went down by $50 million, you sell that position and have a short-term loss of $50 million, which lowers your taxable income by that amount. One day later, you sell the other position, which should be a profit of right about $50 million. The important distinction is that this profit is a long-term profit, taxed at the long-term capital gains rate. If you had a normal income of $50 million during the year, the short-term loss meant you had 0 taxable income, paying $0 taxes. The $50 million long term gain will be taxed at 20%, leaving you with 40$ million a year later. Effectively, you transformed $50 million in ordinary income into $50 million in long term capital gains, saving you $10 million in taxes.

Described like this, it would be illegal. Doing this strategy on a single security, such as stock in a single firm, would break the law and the government would soon be after you. But being very bold and tweaking the formula a bit can save hundreds of millions in taxes. And that is what Susquehanna Fundamental Investments have been doing for a decade.

Instead of betting on and against a single security, the fund spread out its investment across the entire market. It bought large positions in companies across the entire market and then shorted the S&P500 index. While overall the fund lost money, $400 million, it generated $1.1 billion in tax savings, all through the above-described strategy. Netted out, the partners “earned” $700 million through these trades. In more practical terms, they lost $400 million to other market participants and the government lost $1.1 billion in tax revenue.

The eagerness to exploit loopholes and the audacity to do so by barely tweaking an illegal strategy in this case is astounding. And far from the only one instance, Susquehanna has been in legal battles with the IRS over different strategies it pursued multiple times over the years. Jeff Yass, known among his traders for his love of betting, seems to be betting against Benjamin Franklin, that he can continue to exploit loopholes in the tax code to save himself billions without repercussions - that taxes are no certainty in his life. But among billionaires, he is far from the only one to do so.